Minimum car insurance covers damage you cause to others, but leaves you exposed to repair bills on your own vehicle. Here's exactly what you're paying for—and what you're risking—at the cheapest legal threshold.

The Two Core Components of Minimum Coverage

Minimum car insurance in most states consists of liability-only coverage, which includes bodily injury liability and property damage liability. Bodily injury liability pays medical expenses, lost wages, and legal costs when you injure someone in an at-fault accident—up to your policy limit. Property damage liability covers repairs to other vehicles, buildings, or property you damage.

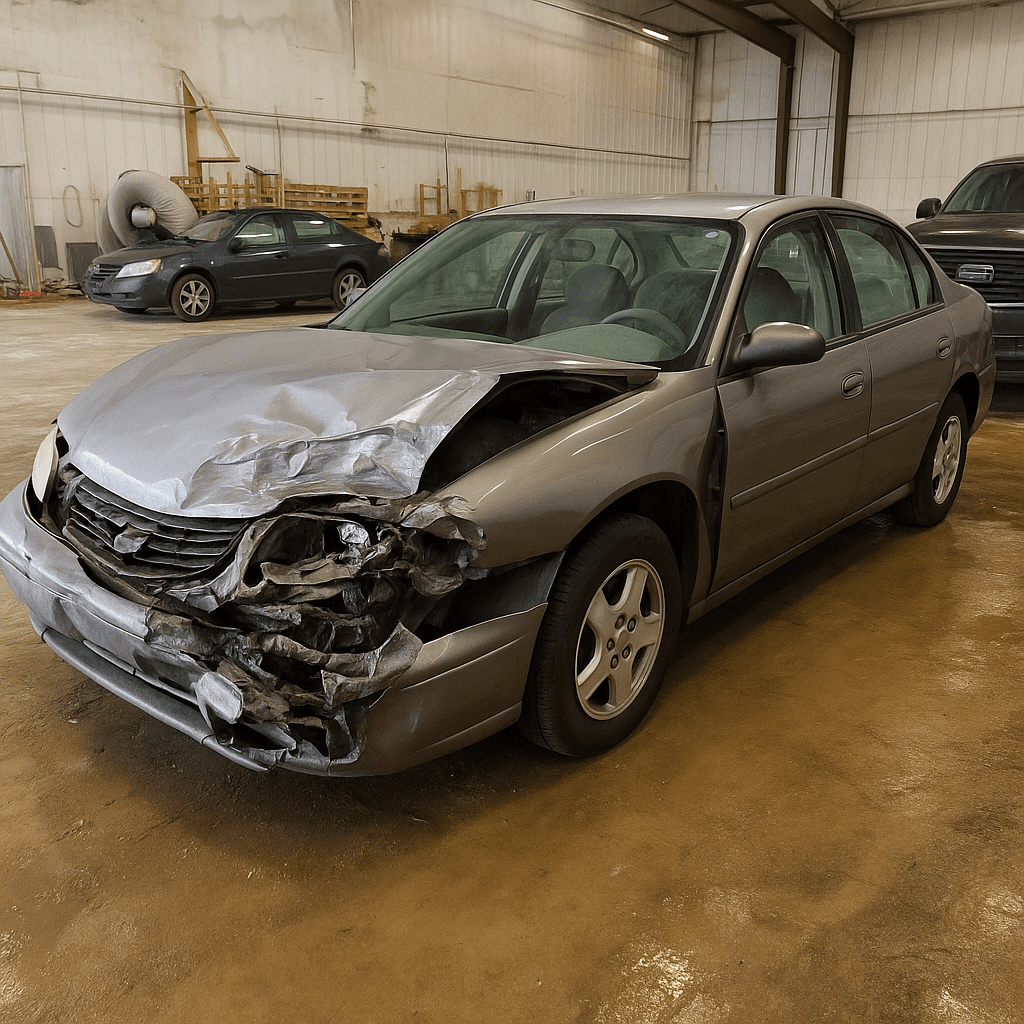

Neither component pays a single dollar toward your own vehicle repairs, your own medical bills if you're injured, or damage from non-collision events like theft or hail. If you cause a $6,000 accident and your car sustains $3,500 in damage, your minimum policy covers the other driver's $6,000 repair bill but you're responsible for your own $3,500 out of pocket.

The most common minimum liability limits are 25/50/25, meaning $25,000 per person for bodily injury, $50,000 total per accident for bodily injury, and $25,000 for property damage. Some states require higher limits—Maine mandates 50/100/25, while California requires 15/30/5. These numbers represent the absolute legal floor, not necessarily adequate protection for most accidents. liability coverage

What You're Not Covered For at Minimum Levels

Minimum coverage excludes collision damage to your own vehicle regardless of fault. If you hit a guardrail, slide into a ditch, or get sideswiped by an uninsured driver who flees the scene, your insurer pays nothing toward your car. For owners of vehicles worth less than $3,000–$4,000, this trade-off is often financially rational since annual collision premiums typically run $400–$800 depending on deductible.

You're also unprotected against comprehensive losses—theft, vandalism, fire, flood, falling objects, and animal strikes. If your car is stolen or totaled by hail, you absorb the full replacement cost. Comprehensive coverage adds approximately $12–$18/mo for older vehicles in most states, but that's still $144–$216 annually that budget-conscious drivers often choose to self-insure.

Minimum policies exclude medical payments coverage and uninsured/underinsured motorist coverage in states where these aren't legally required. If you're injured in an accident you caused, your health insurance handles medical bills—or you pay out of pocket if uninsured. If an uninsured driver hits you, you're left suing them personally for damages your liability-only policy won't cover.

Find the minimum coverage that meets your state's requirements

Compare liability-only rates from carriers in your state — and see what discounts you qualify for.

Get Your Free Quote✓ Minimum Coverage Options✓ No Obligation✓ Licensed Carriers✓ All 50 States

The Financial Exposure Gap You're Accepting

The biggest risk with minimum liability limits is underinsurance in serious accidents where damages exceed your policy caps. The average bodily injury claim for accidents involving injuries was $20,235 in 2022 according to Insurance Information Institute data, but severe crashes easily generate six-figure medical bills. If you carry 25/50/25 limits and cause an accident resulting in $150,000 in medical costs and $35,000 in property damage, your insurer pays the first $50,000 for injuries and $25,000 for property—you're personally liable for the remaining $110,000.

Courts can garnish wages, place liens on property, and seize assets to satisfy judgments beyond policy limits. For drivers with minimal assets, bankruptcy may be the only option after a catastrophic at-fault accident. Raising liability limits from 25/50/25 to 100/300/100 typically costs an additional $8–$15/mo, which represents meaningful budget impact for cost-conscious drivers but also significantly reduces personal financial exposure.

Your own vehicle replacement cost is the other major gap. If you're driving a $4,500 vehicle and total it in an at-fault accident, you're out $4,500 plus the cost of replacement transportation. For households living paycheck to paycheck, this can mean loss of employment access or taking on high-interest debt for another vehicle. The math depends entirely on whether you can afford to replace your car from savings versus whether you can afford $30–$50/mo for collision and comprehensive coverage.

State-by-State Minimum Coverage Requirements

Minimum liability limits vary significantly by state, creating different baseline protection levels. New Hampshire and Virginia allow drivers to operate uninsured entirely under specific conditions, though Virginia charges a $500 annual uninsured motorist fee. Alaska requires 50/100/25, Florida mandates only $10,000 property damage and $10,000 personal injury protection with no bodily injury liability requirement, and Michigan historically required unlimited personal injury protection though recent reforms allow drivers to opt out if covered by qualifying health insurance.

States also differ in whether they require uninsured motorist coverage, medical payments coverage, or personal injury protection as part of minimum policies. In no-fault states like Michigan, Florida, and New York, your own insurer pays your medical bills regardless of fault through PIP coverage, which is mandatory. In traditional tort states, minimum coverage includes only liability and you rely on the at-fault driver's insurance or your own health coverage for injury costs.

Some states explicitly allow lower liability limits for older vehicles or drivers meeting specific criteria, while others maintain uniform minimums regardless of vehicle value. Understanding your state's specific floor requirements determines both your legal compliance cost and the protection gaps you're accepting when you choose minimum coverage.

When Minimum Coverage Makes Financial Sense

Minimum coverage is most defensible for drivers with vehicles worth less than $3,000, no assets to protect from lawsuits, and access to alternative transportation if their car is totaled. If your 2008 sedan with 180,000 miles is valued at $1,800 by Kelley Blue Book and annual collision/comprehensive premiums would cost $600, you'd recover your coverage cost in three years even if you never file a claim—a poor value proposition.

Drivers with qualifying health insurance who live in states with mandatory PIP or medical payments coverage face less personal injury risk from minimum liability-only policies. Your medical bills are covered through PIP up to the state-required limit, and your health insurance handles costs beyond that. The remaining exposure is primarily property damage to your own vehicle and liability beyond policy limits.

The calculation shifts for drivers with home equity, retirement savings, or other attachable assets. A $40,000 net worth makes you vulnerable to collection efforts after an at-fault accident exceeding your liability limits, and the incremental cost to raise limits from state minimum to 100/300/100 is typically $100–$180 annually—cheap protection relative to potential six-figure liability. Minimum coverage is a budget decision, not a universally optimal one.

How to Fill Coverage Gaps Without Full Coverage Costs

If minimum liability feels insufficient but full coverage costs are prohibitive, consider raising only your liability limits while keeping collision and comprehensive deductibles high or excluded entirely. Increasing from 25/50/25 to 50/100/50 costs approximately $6–$11/mo in most states and dramatically reduces personal lawsuit exposure without adding the $40–$60/mo cost of collision and comprehensive.

Adding uninsured motorist coverage provides protection when hit by drivers with no insurance or insufficient coverage, typically for $5–$10/mo. This is particularly valuable in states with high uninsured driver rates—Mississippi, Michigan, Tennessee, and New Mexico all exceed 20% uninsured motorist rates according to Insurance Research Council data. You're effectively paying to insure yourself against others' lack of coverage.

Another option is excluding collision coverage but adding comprehensive-only, which protects against theft, vandalism, and weather damage for roughly $10–$15/mo while avoiding the higher collision premium. This makes sense if you're confident in your driving but worried about environmental risks or vehicle theft. The key is identifying which specific exposures concern you most and paying only for coverage addressing those risks rather than accepting a one-size-fits-all minimum or full coverage package.